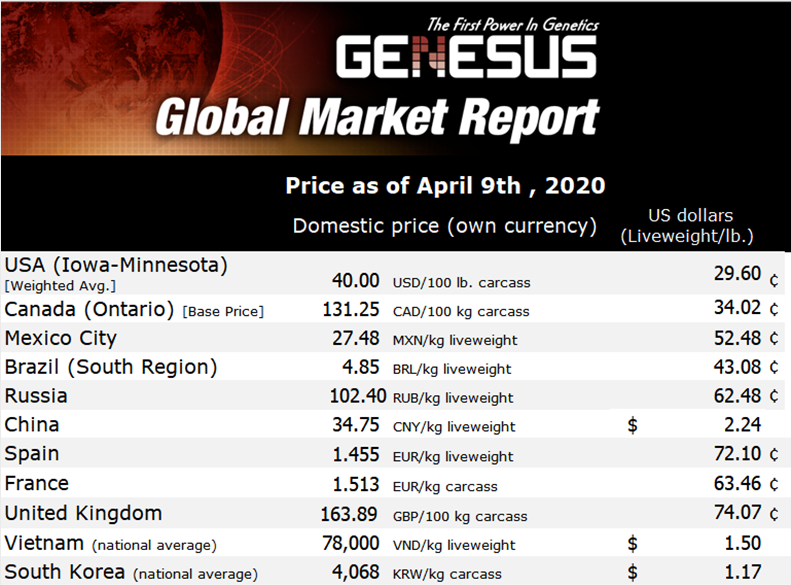

Genesus Global Market Report: USA, April 2020

In my last commentary, I was questioning the CME and its disconnect to the cash hog market, and I would like to continue on that path. 16 April 2020

16 April 2020

3 minute read

3 minute read

By:

By:

A few years ago, actual basis contracts became popular as they were fairly easy to understand and a great way to handle risk management.

I charted the actual basis daily and had about 10 years’ worth of the actual basis numbers. It was fairly predictable. There were times that cash hog basis were historically high, there were times it was an even basis, and at the end of August inverted to the futures. You could bank on it. This is no longer the case. Some could say there is NO connection what so ever between cash hogs and the hog futures.

The basis used to average about $2.00 for the entire year, now it is closer to $10.00! Someone smarter then myself will have to explain why the timing of this change coincides with the time all trading became electronic.

I have studied the CME group which owns the Chicago Mercantile Exchange and the Chicago Board of Trade. Can I say it is unfair? Well no; but The CME Group knows every single sell order and every single buy order and the price of each one as it is all done electronically. It appears to me that it would not be hard to place some bets of your own when targets are hit.

Is the system tilted? Maybe, maybe not but I can say with all confidence that it is not the same since the CME Group took over both trading pits (CME and CBOT) and got rid of the live trading pits. In 2015, floor-based trading was halted and today it is all electronic trading which is mostly based on algorithms. Fundamentals seem to have no relevance at all. The world is short 25 percent of the hogs we once had! And prices continue to slide? I am not sure which algorithm method is used to figure that out.

As I looked into the owners of the CME I found these as the largest owners: Capital Research and Management Co., The Vanguard Group, Blackrock Fund Advisors, SSgA Funds Management Inc., Capital Research and Management Co., Edgewood Management LLC, Fidelity Management and Research Co., Geode Capital Management LLC, and JPMorgan Investment. What is interesting as you look into those groups they seem to own a fair amount of each other. Digging a little more I found out the CME Group has a high percentage of institutional ownership. In general, these are owners and by definition, have a high degree of education and therefore have fewer protected regulations.

So as the rest of the industry is trying to understand how to survive, it appears, The Mercantile Exchange and its electronic trading has few regulations. If I am incorrect in my assumptions I would gladly listen to why I am wrong.

Below is an article summarising the National Cattlemen's Beef Association (NCBA) thought on Futures Market.

NCBA REQUESTS PRESIDENT TRUMP EXPAND USDA MARKET INVESTIGATION, EXAMINE FUTURES MARKETS

Apr. 9, 2020 - NCBA

National Cattlemen's Beef Association (NCBA) reports:

Washington - Today, NCBA President Marty Smith sent a letter to President Donald Trump, requesting the government to act quickly to investigate the striking disparity between boxed beef prices and cattle prices in the futures and cash markets during the current COVID-19 crisis and following the packing plant fire in Holcomb, Kan., last August.

In his letter, Smith requests President Trump to direct USDA to expand the ongoing investigation into market activity after the Holcomb fire to include current market volatility, "in the hope of identifying whether inappropriate influence occurred in the markets, and to provide our industry with recommendations on how we can update cattle markets to ensure they are equipped to function within today's market realities."

The letter also requests the Commodity Futures Trading Commission to study the influence of speculators on live and feeder cattle futures contracts to determine whether these contracts remain a useful risk-management tool for cattle producers.

"Fair and functioning cattle markets are vital to the sustainability of our industry," Smith wrote. He also pointed out the importance of keeping the beef supply chain moving during this time of volatility and instability.

"The market woes for cattle producers will only grow if packing plants shut down or slow down for an extended period," Smith stated. "As cattle producers, we are the beginning of the beef supply chain, and we need continued vigilance and oversight of all cattle market participants - for the benefit of America's cattle producers and all Americans."