CME: Pork Bellies the Bright Spot This Summer

US - Where would the hog market be without bellies this summer? To use an old colloquialism, “Hurting for certain!“ Bellies have been the bright spot among wholesale pork cuts this summer as prices have DOUBLED since mid-May and gained $10/cwt just last week, write Steve Meyer and Len Steiner. 10 August 2015

10 August 2015

2 minute read

2 minute read

By:

By: While fresh belly production has been higher than last year in the same proportion as pork output (+11.7 per cent the past four weeks and +8 per cent year-to-date), this surge of belly prices is being driven by an apparent resurgence of demand as well as the culmination of two years of wild gyrations in frozen belly inventories.

Those inventories got unusually tight back in 2013, pushing belly prices to then-record levels. Belly users apparently vowed to never let that happen again and carried VERY large belly stocks in to 2014.

In fact, monthly belly inventories were the highest of the last 5 years for each respective month from January through October 2014. Those stocks blunted to some degree the impact of PEDv on belly prices last year.

Even though they did set new records in early April, the run-up for bellies prices was much less dramatic than were those of other cuts, especially hams.

That experience seemed to convince the holders of belly inventories to vow to never again have that many in hand and so stocks have been maintained at a more normal — though significantly higher than in 2013 — level this year.

June 30 stocks of 44.47 million pounds were 47 per cent lower than one year earlier but only 14 per cent lower than the 5-year average. So stocks have been tight but not ridiculously so. We think the big issue in this summer’s strength is simply the return of bellies and bacon to more normal prices and the stimulative impact that has had on consumer purchases.

Those high belly prices in 2013 and 2014 had to be passed along to end users and, last we checked, demand curves still slope downward.

Higher prices meant less quantity demanded. That reduction in usage contributed to last year’s inventories and pushed prices sharply lower with USDA’s belly primal composite hitting $63.85 in early April — less than one-third its value one year ago.

But the good news is that demand curves slope downward and bacon is now again a feature item with attractive pricing and, still, tastes better than about anything one can put on a plate. Quality brands of bacon have been on sale in central Iowa at two one-pound packages for $5 in recent weeks and the product movement and tighter freezer supplies have processors once again chasing bellies.

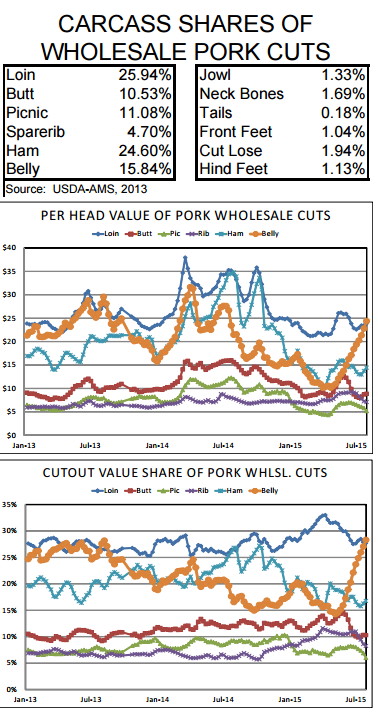

As can be seen at right, the impact has been huge with the gain in the belly composite primal value contributing roughly $15 per head more last week than at the end of April (top chart). And it is easy to see the cut that is still dropping the value ball relative to last year: Hams! They are worth only about $15 per head now where they were contributing almost $30 per head last summer and fall.

As of last week, the belly primal was accounting for 28 per cent of the total cutout value on just 15.84 per cent of the total carcass (table). That is the highest share of any cut for the first time since August 2013.

The share contribution of butts, though down in recent months due to export challenges, has been buoyed in recent years by the emergence of pulled pork as a popular food trend. Can we make “pulled ham”?